Why Excellent Credit Is Your Biggest Refinancing Asset (Leverage It)

If you have a credit score of 720 or higher, you already hold the single most valuable card in the student loan refinancing process. Lenders reserve their lowest interest rates for

How to Compare Student Loan Refinancing Offers: The 5 Numbers That Actually Matter

When you start shopping for student loan refinancing, you’ll quickly be presented with rates, terms, and monthly payments from multiple lenders. It’s easy to fixate on

Student Loan Refinancing for Dentists: Managing $280K+ After Dental School

Dental school graduates face one of the largest student loan burdens in higher education. According to the Education Data Initiative, dental school borrowers who graduated in 2025

12 Common Mistakes Borrowers Make When Choosing Student Loans—and How to Avoid Them

This guide outlines 12 common student loan mistakes, emphasizing the importance of comparing federal vs. private loans, fixed vs. variable rates, understanding APR and fees, and us

Score Your Refinancing Goal: Lower Student Loan Rates with a Clearer View of the Field

Admire offers a transparent student loan refinance marketplace with soft credit checks, enabling borrowers to compare pre-qualified rates and lower loan costs confidently while avo

Best Student Loan Refinancing Lenders in 2026: Each are unique

Choosing the right lender is the difference between a good refinancing experience and a frustrating one. We’ve reviewed the most popular student loan refinancing companies in

Can You Refinance Student Loans While Still in School?

In most cases, no — you cannot refinance student loans while you’re still enrolled as a student. The majority of refinancing lenders require a completed degree and proof of

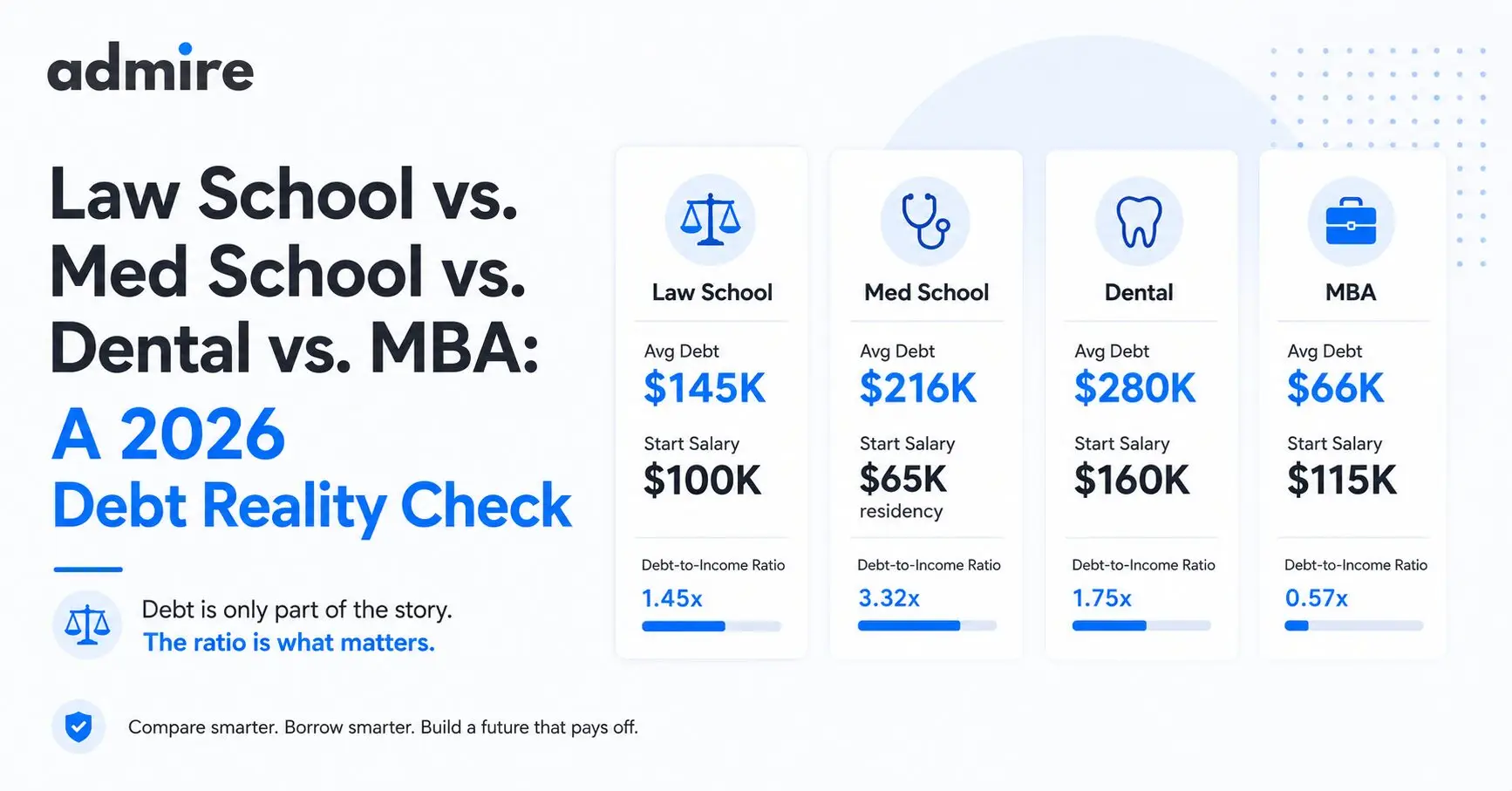

Law School vs. Med School vs. Dental vs. MBA: A 2026 Debt Reality Check

What professional school costs in 2026, what repayment looks like at median salaries, and which debt strategy fits each career path. Side-by-side data.

How Admire’s Soft Credit Checks Protect Your Credit Score

Admire’s soft credit checks let you compare private student loan refinance rates risk-free, protecting your credit score by using prequalified offers without hard inquiries.

The July 1 Deadline: What OBBBA Changes Actually Mean If You Owe $100K+

July 1, 2026 implements every major OBBBA student loan change. If you owe $100K+, here is your situation-specific action plan before the deadline.